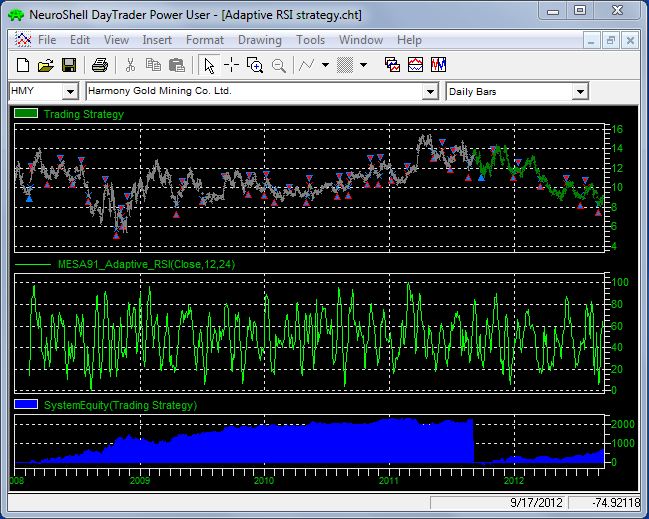

Relative Strength indicators (RSI) traditionally are used to determine when a market is oversold (RSI low) and when it is overbought (RSI high). Traditional RSI Indicators have a lookback parameter, but in MESA91, the lookback is determined dynamically. So our example enters a long trade based on the Adaptive RSI being below a threshold, meaning that the market was oversold. We reversed to short when the Adaptive RSI was above a threshold, meaning the market was overbought. We utilized NeuroShell's optimizer to determine what the thresholds should be. The model was optimized through the end of August 2011, and then tested through mid September 2012. The model held up nicely in the out-of-sample period.